Gain the ability to price physical risk

Nature remains largely external to financial markets, so the ecosystem conditions that shape climate- and nature-related physical risk are still not priced endogenously. TLG’s framework closes that analytical gap by bringing hazard, exposure, ecosystem vulnerability, and sector dependency into one pricing architecture, translating physical risk into conventional financial mechanisms until the market is able to internalise it directly.

Physical risk is mispriced because it is largely absent

Absent from the inputs

Nature is a buffer or an amplifier of hazards

Disclosure without price

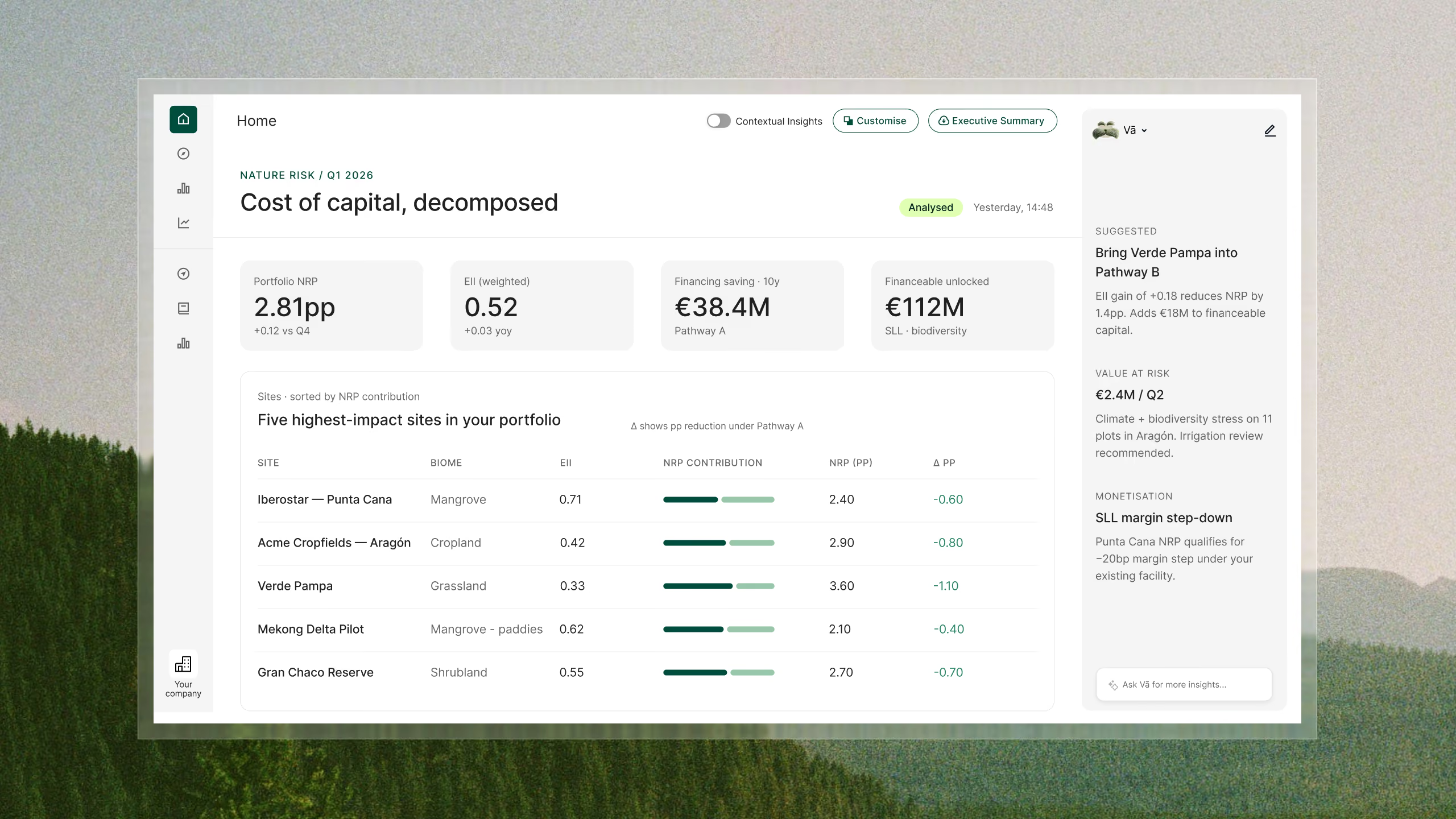

Nature Risk Premium (NRP): The missing term in the cost of equity

NRP is an additive adjustment to the cost of equity within CAPM, calibrated from vulnerability (V = 1 − EII), physical stress (P = Hazard × Exposure) and sector-specific dependency coefficients. It is designed as a transitional pricing signal, correcting for externalities until markets converge to endogenous pricing over time.

V = vulnerability, derived from measured ecosystem integrity

P = physical stress: hazard × exposure

a, b, c = dependency coefficients, calibrated per sector

Nature Risk Adjustments (NRA): the same logic, applied to credit

Debt prices risk through creditworthiness, not premia. The Nature Risk Adjustment (NRA) turns the same inputs into rating adjustments that flow through to credit spreads, collateral haircuts, covenant design and loan tenor.

Sector-calibrated. Because dependency is sector-specific.

NRP coefficients vary materially by sector. The dependency coefficient governs how strongly an industry’s economics are coupled to ecosystem services.

Where it applies

Equity valuation / DCF

Portfolio screening

ESG / sustainability integration

Credit assessment

Credit rating calibration

Loan structuring

Built for you in Landler

The framework runs in Landler, deployed as a custom build. We scope it around your portfolio, your sections, your instruments, and your needs.

Book a consultation